As technology is constantly evolving at a rapid pace, there’s no standing still for businesses wishing to stay competitive in the digital world. The once nice-to-have digital transformation is becoming today an ever-more-important strategy to achieve operational efficiency, profitability, success, and competitive advantage.

The global digital transformation market is expected to grow at a compound annual growth rate (CAGR) of 23.1% from 2022 to 2030 to reach $3,810.05 billion by 2030. These figures alone demonstrate just how fast this trend is seeping into every single industry around the globe. “Digitise to survive” is the buzzword of our era, and digital transformation is the “inevitable reimagining of business” in the years ahead.

In this article, you can explore what digital transformation means for organisations across all industries and sectors and how it drives efficiencies and productivity while enhancing the customer experience. We have gathered all the need-to-know digital transformation statistics, projections, and trends that are gaining momentum today to help you find out what others are doing and what you need to do to stay competitive in the digital era.

Our comprehensive list of digital transformation facts and statistics comes from authoritative sources such as Gartner, Mckinsey, Statista, Deloitte, Harvard Business Review, PwC, etc., with the most up-to-date data. The list is broken down into different categories, so you can focus on what’s most important for your business.

The stats outline both the opportunity and pitfalls of the digital transformation process, which is crucial in assessing your digitisation needs, creating an effective action plan, and better preparing for the future.

What is Digital Transformation?

Digital transformation is today the primary driving force for innovation and operational efficiencies. However, many business leaders are still unclear on what digital transformation means.

If we had to come up with the term, we would probably define digital transformation (DT or DX) as the process of leveraging digital technologies to improve overall business practices, boost customer experience and drive business growth. Fundamentally, DX changes how businesses operate and deliver value to their customers.

Simply put, digital transformation is the step that takes the business world officially into the digital era by forcing organisations to continually challenge the status quo, experiment more, become more agile in their ability to respond to customers and rivals, and get comfortable with failure.

There are many technologies that fall under the digital transformation umbrella, including cloud, artificial intelligence (AI), machine learning (ML), big data, and the Internet of Things (ΙοΤ).

The Importance of Digital Transformation

Not long ago, the COVID-19 pandemic brought new urgency to achieving digital transformation goals, forcing many organisations to accelerate their transformation journey.

Today, digital transformation is imperative for all businesses, from small companies to large enterprises. Every study, research, and article underlines its importance when it comes to how they can remain competitive and relevant as the world becomes increasingly digital.

Some of the benefits of digital transformation include the following:

- Improved data collection

- Higher-quality customer insights

- Better customer experience

- Boosted productivity

- Increased profits

Digital transformation is likely to change the entire market and organisations that fail to build a digital strategy may face the risk of getting left behind.

- 87% of senior business leaders say digitalisation is a company priority, yet only 40% of organisations have brought digital initiatives to scale.

- Data from PwC reveals that 60% of senior executives believe that digital transformation will be critical for business growth this year.

- A study conducted by the Digital Marketing Institute reveals that 1 in 3 companies believe that digital transformation is a matter of survival.

- 56% of CEOs report that their digital improvements have already increased profits.

- In comparison to competitors, companies that adopt digital-first strategies are 64% more likely to achieve their business goals.

- Research shows that digitally mature companies are significantly more likely to have revenues over $1 billion than their digitally novice counterparts.

- CEOs report that digital transformation has the greatest impact on operational efficiency (40%), time to market (36%), and customer satisfaction (35%).

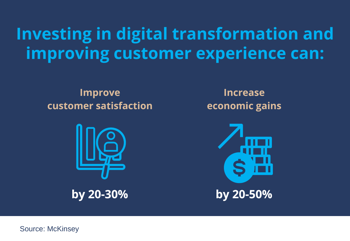

- According to McKinsey, investing in digital transformation and improving customer experience can increase customer satisfaction by 20-30% and increase economic gains by 20-50%.

The State of Digital Transformation Today

In recent years, digital transformation has dominated the conversations around Industry 4.0, and for good reason. Global technological advancements have changed all aspects of life drastically, and the business world is no exception. In fact, the change there is faster, and organisations across sectors are racing to catch up. So, what’s the state of digital transformation in the business world?

- Over 90% of organisations are engaged in some form of digital initiative today, according to Gartner.

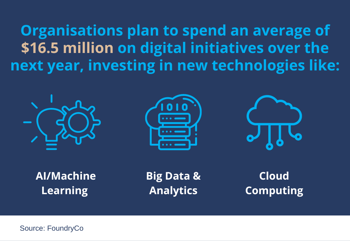

- 89% of all companies have already adopted a digital-first business strategy or are planning to do so. Specifically, organisations plan to spend an average of $16.5 million on digital initiatives over the next 12 months, investing in new technologies such as artificial intelligence (AI)/machine learning (ML), data & analytics, and public cloud.

- To achieve their digital transformation goals, 93% of companies believe that innovative technologies are essential.

- Only 23% of companies are not dependent on digital products or operations.

- Despite the growing awareness of human factors in digital transformation - such as employee experiences and organisational cultures - most transformation efforts continue to focus on modernising customer touchpoints (54%) and enabling infrastructure (45%).

- 70% of respondents to a Thomson Reuters survey indicated that “using tech to simplify workflow and manual processes” to cut costs was a top priority going forward.

- Digital adoption is well underway, with companies making headway in their strategic roadmap. More than 80% of organisations already have a well-defined workplace transformation strategy in place.

- Most organisations (57%) believe digital transformation will have more impact on workplace transformation than physical (38%) and cultural (15%) elements.

- Industry leaders when it comes to digital-first strategies are services (95%), financial services (93%), and healthcare (92%).

Global Key Players in Digital Transformation

Some of the prominent players operating in the global digital transformation market are:

- Accenture plc

- Apple Inc.

- Adobe Systems Incorporated

- CA Technologies

- Dell EMC

- Hewlett Packard (HP) Enterprise Co.

- International Business Machines (IBM) Corporation

- Microsoft Corporation

- Google Inc.

- SAP SE

- Oracle Corporation

- Intel Corporation

- Nvidia Corporation

- Capgemini SE

- Deloitte Touche Tohmatsu Limited

- Salesforce.com, Inc.

- Cisco Systems, Inc.

The Driving Forces of Digital Transformation

Digital transformation market growth is primarily driven by factors such as perpetually growing internet users and smart devices, technological advancements, and government initiatives toward digitisation. In addition, untapped opportunities to enhance sales efficiency, streamline business processes, and take advantage of market dynamics are all contributing to market growth.

- Most digital transformation efforts are driven by growth opportunities (51%), followed by increased competitive pressure (41%). In addition to high-profile data breach scandals, new regulatory standards like GDPR are also motivating organisations to transform (38%).

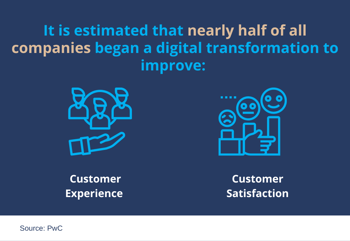

- It is estimated that nearly half of all companies began a digital transformation to improve customer experience and customer satisfaction.

The Role of IT Decision-Makers in DX Success

C-suite executives are also a major driving force behind digital transformation. As organisations’ ability to evolve with the market and continually add value to customers depends critically on technology, CEOs are pivotal to digital transformation success. CIOs are also at the forefront of digital adoption efforts.

- CIOs are reported as most often owning or sponsoring digital transformation initiatives (28%), with CEOs increasingly playing a leadership role (23%), according to Prophet.

- CEOs are driving the development of a workplace transformation roadmap in 45% of organisations and contribute to its development in 63%.

- 97% of IT decision-makers are involved in digital transformation projects.

- The chances of a successful digital transformation are six times greater in organisations with an engaged Chief Digital Officer, according to McKinsey.

- The CIO role was elevated due to the pandemic, and this visibility within the organisation is expected to continue. In fact, 74% of CIOs agree with this statement, and 78% of their LOB counterparts agree.

Investment in Digital Transformation

As technologies continue to evolve and emerge, companies need to keep up by investing in their own transformations. However, striking the right balance in investment between maintenance and innovation will be an ongoing challenge, according to projections. The figures below highlight the significant growth in investment in digital transformation.

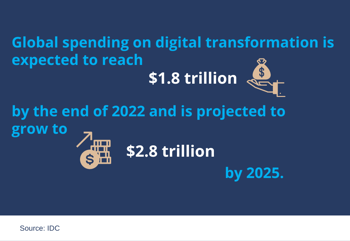

- Global spending on digital transformation is expected to reach $1.8 trillion by the end of 2022 and is projected to grow to $2.8 trillion by 2025.

- Digital Transformation could reach $100 trillion in societal and industrial value by 2025, according to the World Economic Forum.

- 76% of companies are investing in emerging technologies.

- A recent KPMG survey of 2,200 tech executives, including 100 in the UK, revealed that despite rising costs, economic uncertainty, geopolitical instability, and a global talent challenge, businesses are investing heavily in digital transformation and plan to advance in the future.

- The average IT department spends over 50% of its budget on maintenance, according to Deloitte. Only a mere 19% of the budget is allocated to investment in innovation.

- According to a 2021 survey, updating IT infrastructure is the primary driver of IT budget increases. Approximately 56% of organisations plan to increase IT spending.

- Direct digital transformation investment was expected to grow at a compound annual growth rate (CAGR) of 18% from 2020 to 2023. By 2023, it is expected to approach $7 trillion as companies build on existing strategies and investments, becoming digital-at-scale future enterprises.

Digital Transformation Challenges

Digital transformation is already a reality for most organisations, ushering in new ways of doing business virtually. Yet most IT leaders are still struggling with challenges like budgeting, skills gaps and talent shortages, resistance to change, and compliance concerns.

- A survey from PwC shows that 45% of executives think their company does not have the right technology to implement digital transformation.

- Companies report digital transformation is still often perceived as a cost centre (28%), and data to prove ROI is hard to come by (29%). Cultural issues also pose notable difficulty, with entrenched viewpoints, resistance to change (26%), and legal and compliance concerns (26%) stymieing progress.

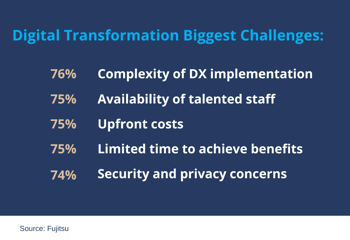

- According to a survey conducted among retailers, the complexity of DX implementation is the biggest challenge overall, with more than three-quarters (76%) rating it as somewhat challenging or highly challenging. The availability of talented staff (75%), upfront costs (75%), the time necessary to achieve benefits (75%), and security and privacy concerns (74%) are also key challenges.

- 76% of CIOs anticipate difficulty in finding appropriate skill sets in the tech areas of cybersecurity and data science in the upcoming years.

- A survey of employees found the most common obstacle to digital transformation was the CEO at 35%.

- 82% of IT security and C-suite executives had at least one data breach attributable to digital transformation.

Reasons Behind Digital Transformation Failure

For businesses across sectors, digital transformation is a primary driver for improved efficiencies and enhanced customer satisfaction. However, not all employers have the necessary skills and knowledge for DX. The employee digital skills gap and the internal resistance to change are probably the biggest challenges companies are facing today – and the main reasons for digital transformation failure.

- It is estimated that 70% of digital transformations fail, most often due to employee resistance.

- According to Forbes, 84% of DX projects fail due to a unidirectional approach to driving such projects and not focusing on all three levers of digital transformation.

- Only 40% overcome the hurdles to create a truly integrated digital transformation strategy: a clear vision backed by a set of strategic imperatives and quantified business outcomes, linking digital to the overall business strategy and sustainable competitive advantage.

- According to a McKinsey study, DX success rates vary by industry and company size. Digitally-savvy industries (like high-tech, media, and telecom) have success rates of 24%, while traditional companies only have success rates of 4-11%.

- A staggering 75% of executives say their business functions compete rather than collaborate on digital projects. As a result, 64% of executives don't see an uptick in revenue growth from digital investments.

- Many organisations are not doing their due diligence when it comes to understanding their customers, with 41% of companies making investments in digital transformation without the guidance of thorough customer research.

The Digital Skills Gap

Businesses face a dual challenge as digitisation advances and new forms of work emerge. On the one hand, they must resolve the issue of the already scarce numbers of experts with technological skills - which are so difficult to recruit for classic industrial businesses and service providers. On the other hand, it is essential that the majority of the remaining workforce be given the new digital qualifications they need in Workforce 4.0.

- A recent Korn Ferry study that includes a sweeping country-by-country analysis finds that by 2030, there will be a global human talent shortage of more than 85 million people, or roughly equivalent to the population of Germany. Left unchecked, in 2030, that talent shortage could result in about $8.5 trillion in unrealised annual revenues.

- By 2030, the U.S. could miss out on $1.748 trillion in revenue due to labour shortages – about 6% of the entire U.S. economy – driven by a shortage of skills, not people.

- Europe also faces a shortage of digital experts: 44% of Europeans between 16 and 74 do not have basic digital skills. According to the European Commission, over 70% of businesses have said that the lack of staff with adequate digital skills is an obstacle to investment.

- Nearly 75% of workers do not feel equipped to learn the digital skills needed now, and 76%, more feel unequipped for the future.

- 50% of the elderly report a lack of digital knowledge and one-third of them a lack of confidence in using tech devices.

- Almost half of the participants in the Global Digital Skills Index see digital sustainability skills as important now or in the next five years. But only 25% say they have the advanced digital skills to promote sustainable business activities.

- A recent Salesforce report found that 59% of hiring managers believe the rise of AI will have a substantial or transformational impact on the types of skills their companies need now and in the future.

- According to PwC, 55% of employers most worried about digital skills say innovation is hampered by a lack of key skills.

- New learning approaches are key to preparing the workforce for technology advancements. Nearly 70% of U.S. hiring managers believe that implementing workforce development programmes will help them prepare for future disruptions or innovations.

- 96% of companies agree they can gain a long-term advantage by investing in the ongoing education of their employees.

Are you struggling to find the best tech talent for your team? We can help. Discover our multi-award-winning recruitment services.

The Impact of Digital on Employees

Apart from the digital skills gap, digital transformation is impacting employees in many other ways. Workers across the globe face problems with work overload, distractions, and access to the right technology and tools. Furthermore, access to high-speed broadband remains an issue for many, and as hybrid working is forecast to grow, this could become a much bigger issue in the future.

Addressing the employee digital skills gap should be a top priority for DX strategies, but so should employee engagement and retention, especially now that the Great Resignation is in full swing. Employee well-being should be at the centre of every business strategy, and the below stats highlight the need for a human-centric approach to transformation.

- According to ScienceDirect, employees face five technology-related pressure points: overload, distractions and interruptions, invasion of personal life, monitoring, and the fast pace of digital work.

- Technology adoption has increased exponentially since the pandemic, setting a new minimum standard for businesses. It is the human element, however, that has proven to be the most effective way of using technology.

- In 2020 and 2021, 48% of organisations stated having invested in cloud-enabled tools and technologies to support their remote workforce. Digital collaboration tools ranked second, which underscores the importance of technologies in empowering a virtual workforce.

- According to Unify Square, in online collaboration tools, 41% of distractions are caused by personal conversations, and 39% are caused by requests that take staff off-task.

- 41% of remote workers experienced cybersecurity incidents when their work setup shifted to a work-from-home arrangement.

- Only 30% of employees say their experience with company technology exceeded their expectations.

- Digital skills are important in today’s workplace. According to World Economic Forum, 54% of all employees will need significant reskilling by 2023.

- 76% of managers agree that companies need to bring people and technology together with more emphasis on the human side.

Industry-Specific Digital Transformation Statistics

Digital transformation is happening at a pace across the globe. The vast majority of organisations already have some digital transformation initiatives in place, but this often means something completely different from business to business, depending on their sector. The way one industry adopts new technologies will be vastly different from another. Here’s what digital transformation currently means for each sector.

- Financial service executives across the world believe enhancing customer experience is the top priority for digital transformation projects: 76% of participants value investing in customers, while 16% prioritise productivity and operational cost reduction in digital transformation strategy.

- The percentage of EU citizens using online banking is expected to double between 2009 and 2029.

- By 2023, chatbots will save banks $7.3 million on annual customer service budgets.

- According to McKinsey, 47% of digital investments made by financial institutions fail to make a greater return than the cost of capital.

- 25% of the insurance industry will be automated in 2025 thanks to AI and machine learning techniques.

- 81% of insurers acknowledge that technology has become an inextricable part of the human experience.

- An average insurer can reduce the cost of insurance by 15-20% with digitisation.

- Fujitsu reports that in retail, the key drivers for digital transformation include: improved competitiveness (70%), reduced costs and increase in efficiencies (69%), stronger customer relationships (69%), improved revenue (67%), enhanced employee satisfaction (60%) and transformed businesses processes (53%).

- According to Gartner, 63% of retailers expect to spend more on business intelligence/data analytics and 35% on artificial intelligence.

- 71% of retailers agree that digital transformation is an essential part of retail technology.

- According to Harvard Business Review, shoppers who use more than four channels spend 9% more compared to those who use only one channel.

- 80% of the customers shop from mobile apps, and customer engagement is maximum from mobile applications.

- The global autonomous vehicles market is estimated to grow to more than $2 billion by 2030, at a 39.1% CAGR. Advanced driver assistance systems combined with a gradual introduction of automated vehicles will prevent 47,000 serious accidents and save 3,900 lives by 2030, and create 420,000 new jobs across automotive, telecoms, and digital.

- Shared mobility through cloud computing and data-driven services could expand Automotive revenue pools by 30% by 2030.

- According to TIM, in the year 2025, there will be an estimated 100 million connected cars. And for Toyota, the challenge for connected cars is receiving and sending large amounts of data to and from the cloud.

- Predictive maintenance based on IoT connectivity tools will enable vehicles to analyse and optimise without human intervention, predict failure in advance and deliver improvements of over 30% in maintenance uptime.

- Automotive leaders believe that by 2025, vehicles will have cognitive capabilities to learn the behaviours of the driver, occupants, and environment to continually optimise. As the vehicle learns more, it will be able to expand its advice to other mobility services options.

- The declining role of fossil fuels is offset by the rapid expansion of renewable energy (wind and solar, bioenergy and geothermal power). The share of renewables in global energy is estimated to increase between 35% and 65% by 2050.

- The increasing importance of renewable energy is supported by the continuing electrification of the energy system. The share of electricity in total final energy consumption will increase from around 20% in 2019 to between 30% and 50% by 2050.

- Energy transition can be achieved through the integration of technologies - such as blockchain and other distributed ledger technologies (DLTs) - with infrastructure. Along with electrification and efficiency enabled by renewables, hydrogen, and sustainable biomass, Infratech is seen by many as a key driver of the energy transition.

- AI will play an essential role in the world’s transition to clean energy. According to Forbes, a switch is taking place away from centralised models of power generation and distribution towards decentralised models.

- By 2030, analysts expect automation to eliminate 29% of jobs while contributing 13% to job creation.

- Data gathered by Statista indicates that 58% of HR leaders use artificial intelligence to improve consistency and quality in their organisations. A further 26% stated that AI is used to assist workers by improving productivity, with the remaining 16% using it to enhance insights.

- 53% of executives and 34% of employees believe that working from home improves productivity.

- 70% of employers intend to engage more temporary workers and freelancers than they had before the pandemic.

- 49% of employees are willing to leave their job if they are unhappy with workplace tech.

- 30% of businesses plan to spend more on cloud, security and risk, networks, and mobility.

- Companies can cut 50% of their real estate costs by going hybrid.

Other Industries

- According to IDG, the top industries for digital-first business strategies are 95% in services, 93% in financial services, and 92% in healthcare.

- Healthcare: Up to $250 billion of current US healthcare expenditure (20% of total expenditure) is available for virtualisation.

- Healthcare: The use of telehealth has increased from 11% to 76% after the pandemic, according to McKinsey.

- Manufacturing: In the manufacturing market, in 2020, digital transformation was valued at $263 billion. It is expected to reach $767 billion by 2026 and work at a growth rate of 19.48% over the forecast period 2021-2026, according to Mordor Intelligence.

Technology-Specific Statistics and Trends

In 2023, companies will continue to invest in technologies like artificial intelligence (AI), the Internet of Things (IoT), cloud computing, big data and analytics, blockchain, and more to optimise operations, minimise efforts, and boost efficiency.

- 31% of organisations predict they will run more than 75% of their workloads in the cloud by the end of 2023, and 20% already do.

- 86% of companies believe cloud technology is critical to digital transformation.

- Globally, the cloud computing market will surpass $1 trillion by 2028.

- Microsoft Azure and Amazon Web Services are the leading cloud storage providers, with over 73% of organisations using them.

- Just 36% of contact centres currently use any form of cloud technology, including software as a service (Saas), hosted, hybrid, and private cloud.

- A European Commission survey of 166 IT leaders shows there are various reasons why enterprises might move their computing to the cloud. The top one, with 61%, is the companies’ cost-cutting initiative. Second comes the desire for new features and capabilities with 57%.

- The implementation of AI will become an increasingly vital business function in 2023. Every day we create roughly 5 quintillion bytes of data, and that number is growing at an exponential rate. But this data is only as effective as the AI systems we use to manage, regulate, and mine it for insights.

- AI will continue to positively affect the customer experience in 2023 and beyond. Gartner predicts that organisations with customer service channels that properly embed AI will experience a 25% increase in operational efficiency.

- By 2027, advanced chatbots will be able to process 95% of customer interactions, cutting human involvement to 5% over the next decade.

- There will be more AI assistants than people in this world. Forecasts indicate that there will be 4 billion AI-powered digital voice assistant units in the world by 2024, which surpasses the total global population.

.png?width=200&height=179&name=Internet%20of%20Things%20(IoT).png)

- The IoT market is currently worth $388 billion and is expected to surpass $500 billion in 2023. By 2030, IoT revenue is projected to surpass $1 trillion.

- IoT devices make our lives more convenient, but they also leave us open to new forms of cyberattack. For those involved in IoT – particularly in the consumer space where networks contain sensitive personal data – spending on security measures is forecast to hit $6 billion during 2023.

- Healthcare is a huge area of opportunity for IoT technology, and the value of the market for IoT-enabled health devices is set to hit $267 billion by 2023.

- A Telecoms survey suggested that the greatest IoT opportunity is smart cities. In total, 81% of respondents believe that IoT can be used to create smart cities, improve traffic management, digital signage, waste management, and more.

- The IoT accounted for the largest share of the overall digital transformation market in 2019. However, AR/VR technology is forecast to have the fastest growth rate until 2025.

- The global augmented reality (AR), virtual reality (VR), and mixed reality (MR) market reached 28 billion U.S. dollars in 2021, rising to over $250 billion by 2028.

- There are an estimated 171 million VR users As of 2022, the VR gaming industry has a market size of $12 billion. 25- to 34-year-olds account for 23% of VR/AR device users. The top barrier to VR adoption is that it's too expensive, with 55% of survey respondents listing this as their hesitation.

- Product placement and advertising is a monetisation method for 47% of VR developers.

- The global Big Data and Analytics market is worth $274 billion. Big Data Analytics for the healthcare industry could reach $79.23 billion by 2028.

- Big Data revenue is expected to double its 2019 numbers by 2027.

- 90% of data globally has been created in the last two years alone.

- Colocation data centres generate over $31 billion in revenue each year.

- 50% of U.S. executives and 39% of European executives said budget constraints were the primary hurdle in turning Big Data into a profitable business asset. Other challenges were data security concerns, integration challenges, lack of technical expertise, and proliferation of data silos.

The Future of Digital Transformation

Digital technologies are already integral to most industries and show no signs of stopping. With that in mind, investing in new technologies like AI, big data, and cloud-based solutions is, in fact, investing in the future.

- The global digital transformation market is expected to grow at a compound annual growth rate (CAGR) of 21.1% during 2022-2027, reaching $1,548.9 billion by 2027 from $594.5 billion in 2022. The main reasons driving the market expansion in the coming years are the rise in the usage of Big Data and other associated technologies, as well as the adoption and implementation of digital initiatives. The introduction of machine learning and artificial intelligence, the rapid development of mobile phones and applications, and the affordability of cloud-based digital transformation solutions are some more significant factors expected to drive market growth during the forecast period.

- Digitally transformed enterprises accounted for $13.5 trillion of global nominal GDP in 2018, but in 2023 they are expected to account for $53.3 trillion, more than half of it. These are signals that a digital economy will soon dominate the global economy.

- At least 90% of new enterprise apps will insert AI technology into their processes and products by 2025.

- Platform-driven interactions are expected to enable approximately two-thirds of the $100 trillion value at stake from digitalisation by 2025.

- 68% of executives believe that collaboration between people and AI will be key to the future of businesses.

- Between 2020 and 2024, global investment in digital transformation will almost double.

The Tech Industry and Workforce in the Spotlight

Disruptive innovation and evolving skills requirements highlight the need for a digitally prepared and educated workforce. Investing in both technology and employees is the key to digital transformation success in any industry.

- According to Forbes, 60% of G2000 companies will use AI or MI-enabled platforms to support the employee lifecycle, from onboarding to retirement.

- By 2023, 70% of employees in task-based jobs will use intelligence within digital workspaces to engage with clients or colleagues from anywhere and to drive productivity.

- The Bureau of Labour Statistics predicts employment in IT will increase by 13% from 2020 to 2030. This is faster than the average for all other occupations.

- 41% of organisations will have a new emphasis on communication and emerging technology skills for remote work, and 42% expect new efforts to upskill and reskill current employees.

- Both the World Economic Forum and McKinsey report that organisations will have increased skills gaps, with employers now looking for workers with critical thinking, analytical and problem-solving abilities, plus adaptability, resilience, and self-management. McKinsey’s survey found that 89% of global companies currently have or expect to have a skills gap.

- Over the next three years, the global workforce can absorb around 149 million technology-oriented jobs.

- According to the European Commission, 90% of jobs are seen to require digital skills in the future.

- Forrester predicts human-centred tech will drive competitive advantage and a 3-5% increase in productivity by connecting the customer experience with the employee experience.

- By 2023, AR and VR in corporate training are expected to total $2.8 billion.

- Over three-quarters (79%) of organisations are pursuing initiatives to address gaps amid a tightening market for IT labour.

The Bottom Line

Digital transformation is set to change how we do business – and for the better. However, along with the opportunities come also some challenges businesses need to overcome to remain competitive in the global marketplace. Embracing the digital era is the first step to success. Organisations across sectors need to invest more in digital technologies, rely more on data-based strategies and adopt a customer-first mindset. By doing so, they can and will thrive.

Labour shortages and digital skills gaps are also major challenges that business and technology leaders need to face. But this is where we can step in. There are thousands of exceptional tech candidates on the market today who have the power to transform your business, and our tech recruitment specialists are up for the challenge of finding the best tech talent for your team.

Templeton holds a 27-year track record of recruiting thousands of I.T. professionals around the globe and a vast database filled with potential candidates that suit your needs. Find out more about our multi-award-winning recruitment services.

Don't miss out on our other market-specific digital transformation reports:

- Digital Transformation in Financial Services Market Report

- Digital Transformation in Energy Market Intelligence Report

- Digital Transformation in Consumer Goods Market Intel Report